Private markets: an update

Private market (PM) investments did not fully realise their potential in the 2025 investment year. While investments in private debt (PD) developed in line with expectations, private equity (PE) investments once again fell short of expectations. Demand for economically resilient and inflation-linked infrastructure investments increased amid volatile capital markets and low interest rates.

For investors reporting in Swiss francs, the abrupt 13% depreciation of the US dollar proved to be a significant drag on performance this year. A promising annual performance measured in US dollars frequently translated into negative returns when expressed in Swiss francs. As the majority of investments within the alternatives and PM universe are denominated in US dollars, Swiss investors face the dilemma of either accepting unhedged USD foreign exchange risk, incurring historically high hedging costs of approximately 4% per annum, or excluding such investments altogether from the outset.

As the CHF share classes of semi-liquid private market investment vehicles are typically currency-hedged, a discount of close to 4% relative to USD performance must be expected, depending on the level of USD exposure within the fund’s investment strategy.

Uncertainty as sand in the gears

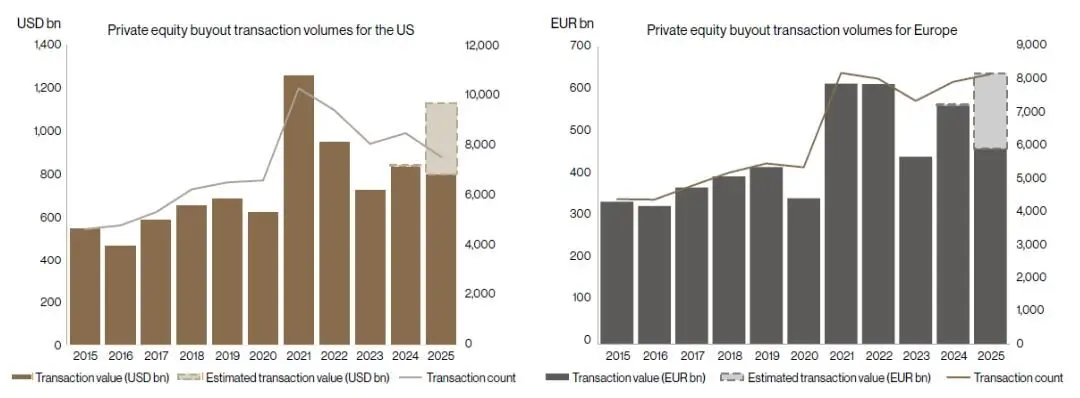

Following the sharp downturns in 2022 and 2023, global exits and IPOs regained momentum in 2024 and 2025, with both volumes and transaction activity increasing. While transaction activity in the U.S. private equity sector is on track for a strong overall year (see left chart), European transaction volumes are expected to exceed even the levels recorded in 2021-2022 (see right chart ).

However, significant frictions remain. U.S. interest rates, which are of key importance for the PM universe, were only further reduced by the Fed in September 2025, as U.S. inflation remained stubborny high. This is significantly later than the market expected at the beginning of the year. As a result, the positive effects of lower U.S. interest rates are expected to materialise only in the coming months. At the same time, trade policy uncertainties (tariffs) continue to weigh on U.S. consumption and investment. In addition, the potentially disruptive impact of artificial intelligence further complicates corporate planning, leading companies to approach major investments or strategic acquisitions with heightened caution at present.

Nevertheless, it is positive to note that the majority of companies continue to exhibit solid fundamental performance and maintain historically low levels of leverage. At the same time, valuations of privately held companies remain attractive relative to those of publicly listed companies.

Private Debt remains attractive

Owing to the delayed reductions in U.S. interest rates, U.S. policy rates have remained at around 4%, while European policy rates stand at 2%. Credit spreads — that is, the premium for assuming credit risk — have declined by around 1% from their 2023 peaks for both private credit and syndicated loans, reaching levels of 5%–5.5% for private credit and around 4% for syndicated loans. From a historical perspective and relative to public high-yield yields, these levels remain attractive.

For investors calculating in Swiss francs, expected returns are lower due to hedging costs, but still attractive compared to the virtually non-existent returns in the CHF bond universe. Especially since, due to the very short duration, hardly any interest rate risks need to be taken into account.

Conclusion

While investments in the private debt universe met return expectations, pri-vate equity investments once again did not meet expectations, particularly for investors with the Swiss franc as their reference currency. We expect the U.S. government to adopt a less confrontational stance in economic policy in the run-up to the midterm elections, which should lead to a partial easing of uncer-tainty. At the same time, U.S. interest rates are expected to continue declining. Both developments are likely to have a positive impact on transaction activity and valuations.

Author: Reto Jung

We are at your service

Your personal partner for all matters relating to your assets.

We look forward to hearing from you!